Around Investment- 2024 In Review; Outlook on 2025 and Beyond

Introduction

- The African investment landscape has undergone significant transformations in 2024, marked by both opportunities and challenges. As we reflect on the year's developments and prepare for 2025 and beyond, this report provides a comprehensive analysis of the investment ecosystem across Africa. It highlights key trends, sectoral insights, regional dynamics, and emerging opportunities that continue to shape the continent's economic trajectory.

- From the dominance of fintech and the growth of climate tech to the persistent gender funding gap and the rise of venture debt, the report delves into the critical drivers influencing investment decisions. It also examines the performance of leading countries, such as Nigeria, South Africa, Kenya, and Egypt, while exploring the potential of emerging markets like Rwanda, Senegal, and Tunisia.

- Looking ahead to 2025, the report underscores the promise of diversification in funding strategies, the continued rise of digital adoption, and the increasing focus on sustainability and innovation. By analyzing these elements, this report provides valuable insights for stakeholders seeking to navigate Africa's dynamic investment landscape.

Funding

- African startups have raised a bit over $2bn year to date and although funding might have crossed the $2bn mark by the end of year, it is evident that the year will close below 2023’s $2.9bn. This is not surprising as it is a reflection of the global downturn in investments following the post-pandemic spike in 2021 and 2022. However, it is safe to say that African startups have been resilient in navigating the funding landscape.

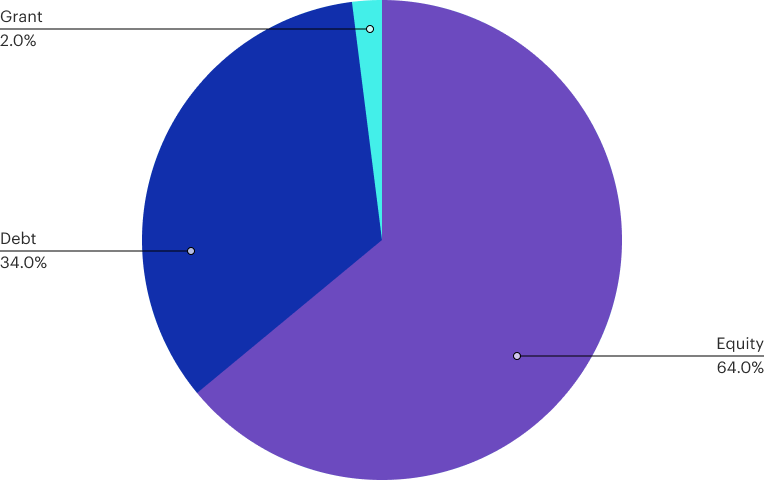

- Equity funding remains the top form of investment, accounting for two-thirds of the total funds raised. Although, as the startup ecosystem is becoming more mature, debt financing is also on the rise without startups defaulting solely to equity financing. According to a report by TheBigDeal, about 68% ($122m) of funding in November alone was in debt. Similarly, AVCA reported about $755 million across 40 deals had been raised through venture debt by October 2024.

- Fintech still attracts the most funding in the African startup funding space, followed closely by energy. Cumulatively, both sectors account for around 64% of total investments in Africa.

- The big four remain the custodian of the majority of 2024 deals in Africa. Nigeria, South Africa, Egypt, and Kenya have remained consistent in leading the funding landscape. Historically, these countries have accounted for two-thirds of total investments and that hasn’t changed in 2024, with Kenya leading the pack this year.

- West Africa has been dethroned by North Africa as the leading region in African VC with US$368 million across 78 deals by year to October 2024. Central Africa is consistently at the bottom of the table with only $6 million raised.

Investment Spotlights

- Nigeria produced yet another unicorn in the startup ecosystem! Moniepoint became Africa’s eighth unicorn following its $110 million series C fundraise led by Development Partners International and other investors like Verod. Google’s Africa Investment Fund, Lightrock. The company has joined startups like MNT Halan, Chipper, Andela, Wave, Opay, Flutterwave, and Interswitch in the big boys’ club.

- Flutterwave received an approval-in-principle from the Bank of Mozambique for its payment aggregator licence and also secured a payment service provider license in Ghana, indicating exciting times for fintech.

- Mobility financing startup, Moove, seems to be on-track to becoming a big boy with its $100 million series B raise which left the company’s valuation at about $750 million. The round led by Uber is to support the startup’s expansion into new markets beyond the six countries where it currently operates.

- 2024 witnessed three of the largest VC rounds in Africa’s history with Showmax (South Africa) raising $177 million, MNT Halan (Egypt) at $158 million, and TymeBank (South Africa) raising $150 million.

- The number of African fintech startups has almost tripled since 2020. According to a report by the European Investment bank (EiB), the number stands at about 1,263 in 2024 compared to only 450 fintech startups in 2020.

- With the rising trends around sustainability, light seems to be shining on the Climatetech space, with over $500 million invested in the space so far. This is more than double the total $217 million investment in 2023.

- Janngo Capital became the largest venture capital firm accelerating gender equality in Africa. The VC raised $78 million which is among the largest raised by an African woman-led investment firm. The raise was oversubscribed by 20% and included investors like the Development Finance Corporation, World Bank’s International Finance Corporation, Mastercard Foundation and the African Development Bank.

- Venture Capitals like Launch Africa, Techstars, 54 Collective, Renew Capital, Baobab Network, DFC; Corporate Ventures like Google for Startups, Microsoft M12; and International Organisations like the Mastercard Foundation, Bill & Melinda Gates Foundation are top supporters of innovation on the African continent.

Key Learnings from Supporting the VC space (By CcHUB)

- The demand for capital and funding continues to dominate the startup ecosystem, particularly for early-stage companies. At CcHUB, we observed that even after securing funding—whether through equity or equity-free funding—many startups return seeking follow-on funding or introductions to additional investors. This trend highlights a persistent funding gap and underscores the need for more robust capital pipelines. For startups, the journey to scalability often requires multiple investment rounds to navigate critical growth stages, from product development to market expansion.

- For sectors like Edtech, investor interest remains low with factors such as extended time to monetization, perceived market risk, and limited investor familiarity with the education sector contributing to low appetite. Educating investors about the potential for impact and scalability is essential.

- Valuation is a key challenge in Africa's startup funding landscape, often complicated by the lack of adequate data points. Many startups struggle to substantiate their valuations due to limited historical performance metrics, inconsistent financial reporting, and a shortage of comparable exits in the region. This data gap makes it difficult for investors to accurately assess risk and potential, often leading to conservative or undervalued assessments. Conversely, some startups inflate valuations based on global trends rather than regional realities. Addressing this issue requires better data collection, transparency, and ecosystem support to establish benchmarks and foster sustainable investment practices.

- Gender disparity remains a big issue with less than 4% of funding raised by all-female founder startups, with most funding through accelerators and incubator programs. Despite evidence that women-led startups often outperform in terms of revenue and impact, systemic biases and limited access to networks hinder their ability to secure funding. Many investors gravitate towards male-led ventures, perpetuating gender imbalances in the ecosystem. Additionally, cultural norms and societal expectations often limit women's participation in entrepreneurship. Addressing this disparity requires targeted interventions, such as gender-lens investing, mentorship programs, and greater representation of women in decision-making roles within the funding ecosystem.

- Most startups at the foundational stages of their development like the ones we support within the CcHUB ecosystem grapple with setting up solid operational frameworks, recruiting the right team and establishing effective governance. These gaps often hinder their ability to scale efficiently or attract investment. To address these challenges, we provide tailored advisory services, helping startups refine their operations, strategize for growth, and adopt sound governance practices. Additionally, our network of customers and partners offers startups the critical connections needed to test their solutions, acquire early adopters, and build credibility in the market.

2025 Outlook

- We can expect an increased diversification of funding with debt financing on the rise. Venture debt will continue to offer a lifeline to startups that intend to ride out the downturn wave. Debt financing could serve as a strategic buffer, helping companies manage cash flow and sustain operations during challenging times. By leveraging venture debt, founders can secure the flexibility needed to make critical decisions, maintain growth trajectories, and adapt to market changes.

- Africa’s investment landscape has been dominated by regional leading markets like Nigeria, Kenya, South Africa, Egypt, Ghana, and Rwanda which have attracted global attention. However, other countries such as Senegal, Uganda, Tunisia, and Mauritius are beginning to stand out as new investment spots. These emerging markets are benefiting from growing entrepreneurship that are creating new opportunities for investors, improved regulatory environments, and government incentives. Investors are beginning to look beyond the traditional leaders, discovering new opportunities across the regions. With its rich diversity and strong drive for growth, Africa continues to rise as a key player in the global economy.

- According to Google’s Public First report, a transformative digital decade is the outlook for Africa. Over half of the region’s population is expected to gain internet access for the first time, driving widespread adoption of emerging technologies like artificial intelligence and cloud computing. These advancements are poised to accelerate economic and societal development across the continent. The report also suggests that every $1 invested in digital technology in Sub-Saharan Africa would generate over $2 in economic value by 2030, unlocking immense opportunities and fuelling growth.

- The African Climate tech sector experienced major growth in 2024 with over half a billion dollars raised, This is more than double of 2023’s total funding. This trend highlights an emerging shift in the funding landscape, signaling growing investors' confidence in renewable energy, sustainable agriculture, and mobility solutions. In 2025, the sector is likely to experience continued growth as it builds on the current funding momentum. This will ultimately set the stage for long-term investments and socioeconomic development across Africa. However, the sector must address challenges like aligning innovations with Africa’s unique market conditions to ensure sustainable growth.

Sources: TheBigDeal, AVCA, EiB, Technext24, weetracker, Tekedia, Lucidity Insights, Briter Bridges, CcHUB Insights