Around Investment (2025 in Review: Outlook on 2026)

Introduction

- Africa's investment story in 2025 wasn't about a single blockbuster round or a headline recovery but about a maturing market.

- After three consecutive years of funding declines, venture capital returned with discipline in 2025. We didn't see the euphoria of 2021 or the overcorrection of 2023; instead, investors backed fewer and bigger bets. For the first time in a decade, debt financing crossed $1 billion, signaling a structural shift in how African startups are choosing to grow.

- Strategic partnerships, consolidation, and efficient use of existing infrastructure defined 2025 in a market moving beyond boom-or-bust cycles.

Funding

- African tech investment recovered in 2025 with venture capital investment reaching $4.1 billion across 570 disclosed deals, a 25% increase from 2024 though still below the 2022 peak of $5.3 billion.

- Recovery wasn't uniform. Q1 slowed under the weight of global economic instability, but markets rebounded from Q2 onward and sustained momentum through year-end. More importantly, the quality of capital improved. Pricing discipline tightened, subsidy-dependent models fell out of favor, and controlling burn rate became a competitive advantage.

- As funding rounds got larger and more concentrated, investors shifted from funding early experimentation to scaled category leadership. Fintech retained its dominance, but Energy, Healthtech, and Proptech claimed a growing share of capital and attention.

- One persistent gap remained: women-led startups continued to receive a disproportionately small share of funding. Precise figures varied by source, but the directional reality was that female founders faced a structurally harder fundraising environment, with limited improvement from prior years.

Highlights

Debt Becomes a Core Growth Tool

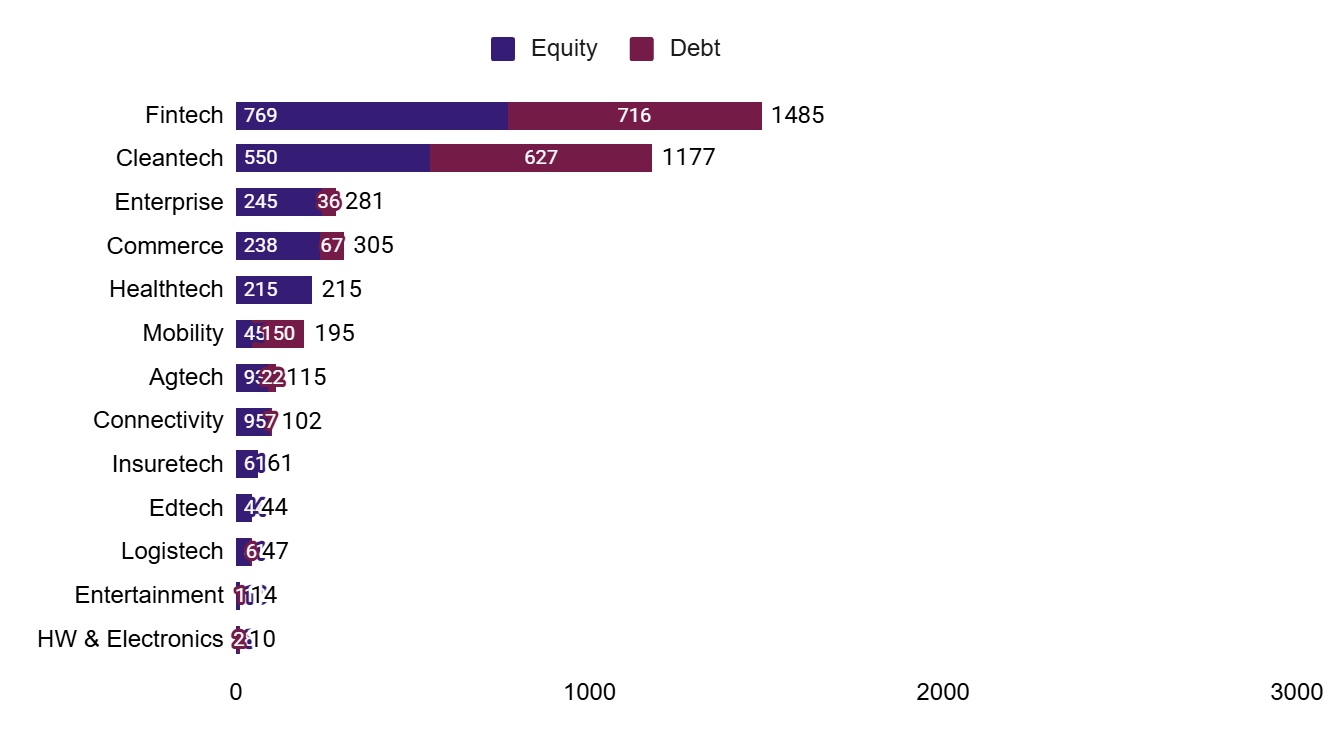

- Debt financing became a mainstream funding tool in 2025, hitting a new high of $1.64 billion—a 63% year-on-year increase. The majority of this capital was hard debt rather than convertible notes (or debt) and was primarily provided by private credit funds, DFIs, and specialist fintech lenders, rather than traditional banks, highlighting the growing maturity of Africa's private credit market and debt's role as a core non-dilutive growth instrument.

- Founders with predictable revenue streams and asset bases are choosing non-dilutive capital deliberately and the infrastructure to provide it is deepening. Fintech and cleantech accounted for over 80% of debt volumes in 2025, but the expectation is that other sectors will begin accessing structured debt as their revenue models stabilize.

Sector Diversification Beyond Fintech

- Fintech remained dominant in 2025, capturing 44% of total debt and a substantial share of equity. Cleantech emerged as a genuine rival for equity and in debt financing, it surpassed fintech entirely. Enterprise, e-commerce, and healthtech maintained steady equity activity at scale.

- Investors no longer need a fintech angle to justify a significant African tech allocation. The universe of fundable, defensible businesses has expanded, and the capital is beginning to follow.

Francophone Africa's Rise

- Among smaller markets outside the Big Four, Francophone Africa dominated, securing 68% of funding ($257 million) and 64% of deals in that segment. The drivers are stronger GDP growth trajectories, the relative stability of the CFA franc compared to the naira or Egyptian pound, and government policies that have been more proactively supportive of tech ecosystem development.

- Senegal's rise to fifth place on the continent is the headline example, but Morocco, Côte d'Ivoire, and Benin are building ecosystems with genuine depth.

Regional Highlights

- Africa's four largest startup markets—Nigeria, Kenya, South Africa, and Egypt—captured 71% of all funding in 2025. Their pull on large deals was even stronger: the Big Four accounted for 81% of rounds above $10 million.

- For rounds under $1 million, the Big Four's share dropped to 56%. Early-stage activity is spreading and startup formation is no longer concentrated in four countries.

- Francophone Africa was the standout among smaller markets, securing 68% of non-Big Four funding ($252 million) and 64% of deals in that segment. Stronger GDP growth, CFA franc stability, and proactive government policy are compounding into a regional advantage that is showing up in the numbers. Angola and Gabon attracted their first-ever venture deals in 2025, modest in scale, but meaningful as signals.

- The continent's funding distribution, however, remains uneven and twenty-six countries recorded no significant deals above $100,000.

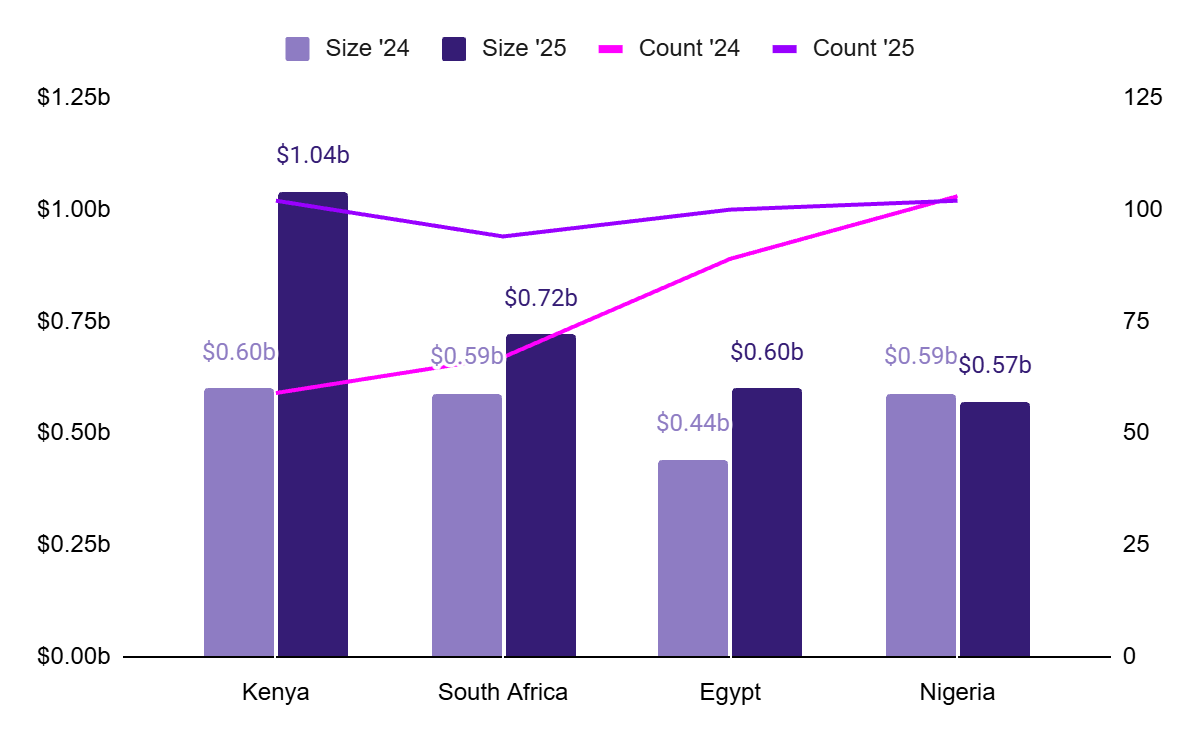

Big Four Performance

Kenya

- In 2025, Kenya was Africa's top destination for startup funding, raising over $1 billion—a 72% surge from the previous year. Growth was propelled by four of the continent's nine megadeals (rounds exceeding $100 million), which together accounted for roughly 60% of total funding.

- The country secured nearly $500 million in debt financing, more than double Egypt's total. It's a reflection of Kenya's capacity to absorb large, asset-backed capital commitments. Venture debt providers and equity investors found a market that could take on serious capital and deploy it into businesses with stable revenue models.

- Kenya's momentum lifted the East Africa region, making it Africa's leading investment destination for the first time. Kenya is cementing its credentials as a scaling hub, with later-stage capital increasingly drawn to proven models in climate tech, fintech, and agritech.

South Africa

- South Africa raised $715 million in 2025, with equity doing the heavy lifting at $643 million across 85 transactions, a contrast to Kenya's debt-led story. Debt funding fell 45%, making up just 10% of the total.

- The sectoral spread stood out. Fintech remained relevant (Optasia raised $345 million while Lula closed $100 million), but significant capital went into energy, healthtech, AI, and agritech. This diversification is a marker of maturity and investors no longer need fintech as the default entry point into South African tech.

- Improved fiscal stability and a recovering international standing have gradually restored investor confidence. South Africa's ecosystem is better-positioned today than it was two years ago, and the fundamentals: infrastructure depth, institutional investor presence, and deal-structuring capability, support that trajectory.

Egypt

- Egypt's 2025 story is fundamentally about currency and cost arbitrage. Egyptian startups raised $604 million, a 37% increase year-over-year as the Egyptian pound lost half its value against the euro over three years. It made local engineering talent, particularly in software and deep tech, among the most competitively priced on the continent.

- Export-focused models proliferated, as startups pivoted toward dollar-denominated revenues to offset constrained local purchasing power. The government reinforced this direction, positioning tech as a key export sector and simplifying the regulatory environment to attract aligned capital.

- Deal activity concentrated in larger rounds: Nawy's $75 million raise and InfiniLink's acquisition by GlobalFoundries were the headline transactions. Egypt recorded 12 acquisitions, the highest of any African market in 2025, indicating the exit environment is developing real depth.

Nigeria

- Nigeria remained Africa's most active startup market by deal count in 2025, recording 102 transactions. By almost every other metric, it was a difficult year.

- Total funding fell 3% to $572 million, driven by a 22% decline in equity investment. Nigeria's share of continental funding dropped to 14%, its lowest since systematic tracking began in 2019. The causes are well-understood: currency volatility, inflation, foreign investor caution around capital repatriation, and an absence of major exits that would otherwise restore confidence at the growth stage.

- Early-stage interest held. Fintech, healthtech, and the creative industries continued to attract seed-stage capital. Government programs like iDICE are working to expand access for underserved founders. For Nigeria to reclaim its position as Africa's anchor market, it needs a meaningful exit: a large acquisition or public listing that demonstrates returns are possible.

Sector Insights

Cleantech Almost Over-taking Fintech

- Renewables and cleantech was the year's most important story. The sector raised $627 million and came within striking distance of overtaking fintech by year-end, a position that would have been unthinkable three years ago. What made this growth structurally distinct was its financing composition: debt surpassed equity, making cleantech the only major sector where that was true. This reflects the nature of the assets being funded: large, physical infrastructure projects with predictable cash flows that suit debt structures better than equity.

- D.light's $300 million raise for off-grid solar and Sun King's $156 million local-currency securitization were the defining transactions. Africa's energy access gap is vast, and 2025 showed that patient capital has found a mechanism to address it at scale.

Fintech: Sustaining Scale, Shifting to Infrastructure

- Fintech held its position as Africa's most-funded sector in 2025, raising $1.49 billion, approximately 38% of all startup funding on the continent.

- Deal volume dipped slightly, but the sector's strength was about scale. Large equity and debt facilities anchored the year, with Zepz pulling in $165 million for cross-border payments and Wave closing $137 million for mobile money. The clearest signal from 2025 fintech investment is that investors are doubling down on infrastructure-layer businesses with proven revenue models and high switching costs.

The Fundamentals Take Hold: Second-Tiers Finding Their Stride

- Enterprise and E/M/S Commerce raised nearly $600 million, confirming their place as a durable second tier of African tech investment. Enterprise funding grew 43% to $274 million, driven by demand for B2B SaaS and logistics infrastructure as African businesses look to digitize operations rather than build from scratch. This is the kind of structural investment that compounds and 2025 suggested investors are paying closer attention to it. E-commerce and marketplace funding reached $312 million across fewer but larger deals, pointing toward consolidation. The era of funding many competing platforms in the same vertical appears to be closing; capital is now concentrating behind the players most likely to own their categories.

- Healthtech had a breakout year, raising $224 million, a 50% increase from the prior year. South Africa's LXE Hearing ($100 million) and Ghana's mPharma ($23 million) led the sector, with investment flowing into telemedicine, AI-assisted diagnostics, and healthcare infrastructure. Africa's healthcare deficit is significant, and investors are beginning to treat it as an opportunity. The rising deal count matters as much as the capital figure, suggesting the pipeline is broadening, not just deepening around a few known names.

- Mobility continued to attract meaningful investment, with investment flowing into ride-hailing, electric vehicles, and vehicle financing. Benin's Gozem raised $30 million, and Rwanda's Spiro closed $100 million, the largest single investment ever made in Africa's electric vehicle sector. The mobility opportunity in Africa is structural: urban populations are growing, petrol costs are high, and alternatives are few. Spiro's model is instructive; its bikes are priced 40% cheaper upfront than petrol equivalents, with 30% lower operating costs. AgTech raised $169.5 million, with 76% concentrated in the Big Four markets.

- Capital shifted toward startups with demonstrable profitability paths with Egypt's Tagaddod ($26 million) and Nigeria's Koolboks ($11.2 million) among them. The sector is moving away from software-layer experimentation toward climate-resilient, operationally grounded solutions. Investors appear to have lost patience for AgTech that cannot show a clear line to unit economics.

Exits/Investors

- The buyer profile in Africa's M&A market shifted in 2025. Global acquirers remained selective and cautious and the active buyers were African: regional banks, telcos, and scaled startups acquiring tech firms to accelerate their own digital transformation. Private equity played a growing role as an exit mechanism for early investors looking to realize returns without a public listing.

- 48 M&A transactions were recorded in 2025. Fintech dominated, accounting for 20 of those deals. Moniepoint's acquisition of Sumac Microfinance Bank was notable, a fintech moving deliberately into traditional banking infrastructure, alongside Stitch's acquisition of ExiPay and C-One's acquisition of Bankly. These deals showed scaled players absorbing capabilities and customer bases to entrench their positions before the next competitive cycle.

- The broader signal suggests returns no longer depend primarily on a foreign acquirer or a cross-listed IPO. Regional capital is increasingly capable of providing liquidity and as that capability grows, so does the investment case for getting into African tech earlier.

Investment Spotlights

- Three deals stood out in 2025 for what they demonstrate about where African tech is maturing fastest.

Sun King (Kenya – Off-grid solar)

- Sun King closed two landmark transactions in 2025. The first was a $156 million local-currency securitization, the largest of its kind in Sub-Saharan Africa outside South Africa, structured to finance solar kits for 1.4 million households. The second was a $40 million growth equity round from Lightrock later in the year.

- Securitizing in Kenyan shillings removes foreign exchange risk from the equation for borrowers and demonstrates that African capital markets can structure sophisticated instruments for infrastructure-scale deals without routing through hard currency. Sun King currently installs 330,000 solar systems per month, with a target of one million monthly installations by 2030. The 2025 financing puts that target within reach.

Moniepoint (Nigeria - Fintech)

- Moniepoint raised an additional $90 million in Series C funding in 2025, bringing its total Series C to over $200 million. The round was led by LeapFrog and included Visa, Google, and the IFC signalling commercial confidence and development finance validation.

- The capital will fund expansion across Africa and the continued build-out of its business banking platform. Moniepoint is one of the few Nigerian startups to sustain unicorn status through a period when investor confidence in the market broadly declined. Its ability to raise at scale in 2025, despite Nigeria's difficult funding environment, is a direct reflection of what strong unit economics and demonstrated retention can do for a company's fundraising leverage.

Spiro (Pan-African - Electric Mobility)

- Spiro raised $100 million in 2025, the largest single investment in Africa's electric vehicle sector to date. The anchor commitment of $75 million came from Afreximbank's FEDA, a signal that development finance institutions are prepared to back physical infrastructure plays at a meaningful scale.

- Spiro operates the continent's largest battery-swapping network, supporting over 60,000 electric motorcycles. Its cost structure is its competitive moat: bikes priced 40% cheaper upfront and 30% lower in operating costs than petrol alternatives.

Investment Outlook

- 2025 established a new baseline. Capital discipline, sector focus, and debt sophistication are now table stakes in African tech, not differentiators. What happens in 2026 will determine whether these foundations support durable growth or simply reflect a market that has learned to survive lean conditions without learning how to scale through them.

- Several dynamics are worth watching.

- Nigeria's recovery will be one of the year's defining stories. The country has the continent's deepest startup pipeline and its highest deal volume. What it lacks is a major exit. A significant acquisition or public listing would do more for Nigerian investor confidence than any policy intervention, because it would demonstrate that returns are real. Without it, growth-stage capital will continue to look elsewhere.

- Kenya's momentum is real, but concentration risk is worth monitoring. Four megadeals drove roughly 60% of its 2025 total. The ecosystem's depth beyond those flagship companies will be tested as capital looks for its next set of bets.

- AI will increasingly shape how capital is allocated across the continent both as a sector in its own right and as an infrastructure layer that affects every other sector. African tech has so far been a late adopter of the global AI investment wave, but 2026 is likely to see that change, particularly in fintech, healthtech, and enterprise software where AI-driven efficiency gains translate directly to unit economics.

- Debt markets will continue to develop. As more African startups reach revenue maturity, the pool of businesses capable of accessing structured debt will expand. Will local capital markets develop the instruments and risk appetite to meet that demand domestically, or will it remain dependent on international DFI participation?

- The gender funding gap remains structurally unresolved. Women-led startups continued to receive a disproportionately small share of capital in 2025, with no meaningful improvement from prior years. This is a missed opportunity and a market inefficiency and 2026 will test whether the commitments made by investors and ecosystem builders around gender-lens investing translate into measurable outcomes.

- Africa's tech ecosystem in 2026 needs to show that its best companies are capable of generating real returns at scale. The infrastructure is improving. The talent is deep. The question is exits, and answering that question will shape the next funding cycle more than any other single variable.

MARKET SPOTLIGHT: RWANDA

Market Overview

- Rwanda punches above its weight. A landlocked country of 14.1 million people with a GDP of approximately $14 billion, it has spent the past decade building a reputation for governance stability, regulatory clarity, and deliberate digital transformation that is disproportionate to its market size. For investors, that reputation is both an asset and a question mark. The same centralized authority that enables rapid policy execution also concentrates risk in ways that require clear-eyed assessment.

Demographics & Consumer Profile

- Rwanda's population is young, with a median age of 20 and a mean of 24.6. Only 4.2% of the population is 65 or older, a demographic profile that implies long-term labor force growth and a consumer base that will expand in size and purchasing power over time.

- Urbanization is still early: approximately 17.8% of the population lives in urban areas as of 2023. The government's National Urbanization Policy targets 52.7% urban by 2035 and roughly 70% by 2050. Those targets imply substantial infrastructure demand, growing consumer markets, and rising digital service adoption over a multi-decade horizon. Mobile internet penetration reached 38% in 2025, significant progress, though still leaving substantial headroom for expansion.

Startup & Funding Landscape

- Rwanda's startup and innovation ecosystem has expanded steadily, supported by direct government intervention, development finance support, and a growing presence of regional and international investors. A key initiative is the Rwanda Innovation Fund (RIF), a government-backed fund established in partnership with the African Development Bank (AfDB) and managed by Angaza Capital, which aims to support up to 150 companies across early and growth stages. Complementary public programs such as Hanga Venture Ignite, the National Fintech Strategy, and targeted innovation grants have further strengthened the early-stage funding environment.

- Private capital participation has increased alongside public efforts. Rwanda has seen growing activity from venture capital firms including Africa Climate Ventures, Afrikev Ventures, Zagadat Capital, In10nsity, and Legacy Invest, while structured angel investing is developing through the Rwanda Angel Investors Network (RAIN). Startup formation and investor readiness are further supported by a network of accelerators and innovation hubs, notably 250STARTUPS, Norrsken Kigali, Impact Hub Kigali, and Westerwelle Startup Haus, which provide capital access, technical support, and regional market connectivity.

- Sectoral activity remains concentrated in fintech, healthtech, agritech, and mobility, reflecting both domestic demand and policy priorities. While capital availability has improved, a persistent pre-seed and seed-stage funding gap remains, particularly for first-time founders without grant or accelerator backing.

- According to StartupBlink, Rwanda hosts 77 startups, representing approximately 6% of Eastern Africa's startup ecosystem. The ecosystem ranks 96th globally, 12th in Africa and 3rd in Eastern Africa, recording 3.9% annual growth and improving its global ranking by two positions year-on-year. Although Rwanda remains a relatively small market, its upward trajectory, institutional support, and regulatory predictability continue to strengthen its appeal as an emerging innovation hub.

Rwanda's Outlook

- Rwanda's outlook remains broadly positive, supported by services-led growth, and continued government focus on digitalisation, innovation, and infrastructure. A young population, rising urbanisation, and targeted support for priority sectors such as fintech, agritech, and healthtech are expected to sustain medium-term growth, while regulatory clarity and institutional backing continue to differentiate Rwanda within East Africa.

- However, growth prospects remain constrained by structural vulnerabilities, including high import dependence, foreign-currency exposure, and elevated public debt levels. While macroeconomic stability is likely to be maintained, exchange-rate movements and fiscal pressures will remain key variables for investors to monitor. Overall, Rwanda presents a policy-driven investment environment with selective opportunities for aligned capital, alongside risks that require disciplined currency and regulatory risk management.

Sources: African Development Bank, Fitch Ratings, International Monetary Fund, National Bank of Rwanda, National Institute of Statistics of Rwanda, S&P Global, Startup Blink, Statista, World Bank, xe.com.

Contact: syndicate@cchub.africa